When it comes to understanding personal finance, some terms can feel confusing or intimidating, and one of the most common is APY, or Annual Percentage Yield. I remember the first time I encountered it, and like many others, I had questions: What exactly does APY mean? How does it affect my savings, investments, or interest earnings? If you’ve ever wondered about APY, you’re in the right place. In simple terms, APY reflects the total interest you can earn on an account over a year, taking into account compounding, which makes your money grow faster than simple interest alone. By understanding how APY is calculated and why it matters, you can make smarter decisions about where to save or invest, compare different accounts effectively, and maximize your earnings without unnecessary confusion. This guide will break down APY in a clear, easy-to-follow way so you can confidently manage your finances and get the most from your money.

What Is APY?

APY, or Annual Percentage Yield, is a key financial concept that helps you understand how much your money can grow over the course of a year when saved or invested. Unlike a simple interest rate, APY takes into account the power of compound interest, which means your earnings don’t just come from your initial deposit. If you’ve ever opened a savings account, certificate of deposit (CD), or invested in another financial product, you’ve likely noticed APY listed alongside the interest rate. This percentage gives you a clearer picture of your potential earnings by showing the total interest you can expect to earn in a year, including the effects of compounding. By understanding APY, you can compare different accounts more effectively and make smarter decisions about where to save or invest your money.

The concept of compounding is what sets APY apart from simple interest or APR (Annual Percentage Rate). With compounding, the interest you earn on your initial deposit begins to generate its own interest, creating a snowball effect that can significantly increase your overall returns over time. APR, on the other hand, only reflects the interest calculated on your original principal, ignoring the interest-on-interest effect. By using APY as a benchmark, you get a more accurate view of how your money will grow and can plan your savings or investment strategy accordingly. Over time, even small differences in APY can lead to meaningful growth, making it an essential factor to consider when choosing financial products or planning your long-term wealth.

Why Does APY Matter?

You might be wondering, “Why does APY really matter?” The answer is simple: it shows you the real return on your money. Whether you’re saving in a savings account, investing in a certificate of deposit (CD), or putting money into another financial product, APY tells you how much you’ll actually earn over time, accounting for the effects of compounding interest. This makes it an essential tool for comparing different financial products accurately. Without considering APY, you might think one account is better based solely on its stated interest rate, when in reality, another account with compounding could give you a higher overall return. By paying attention to APY, you can make smarter, more informed decisions about where to place your money to maximize growth.

For example, imagine you’re comparing two savings accounts: one offers a 2% interest rate, while another offers 1.95% interest but compounds daily. Due to the compounding effect, the account with the slightly lower interest rate could actually provide a higher APY, meaning you’d earn more over the course of a year. From personal experience, monitoring APY has helped me significantly boost my savings. When I opened a high-yield savings account, I carefully checked the APY to ensure I was getting the most value. Once you start using APY as a comparison tool, it becomes clear how powerful it is for making smart financial decisions and maximizing your returns over time.

See; What Is a Savings Account and How Does It Work?

The Difference Between APY and APR

You may have also heard of APR, or Annual Percentage Rate. It is easy to confuse APR with APY, but they are not the same. The key difference is that APY includes compound interest, while APR does not. APY shows how much your money can grow over time. APR usually describes the interest you pay on a loan, credit card, or mortgage. For example, a loan with 5% APR means you pay 5% of the loan amount in interest over one year. It does not account for compounding. Understanding this difference is important for making smart financial decisions.

When you are saving or investing, APY is the term to focus on. It tells you the actual earnings on a savings account or investment, including compounding. If you are borrowing money, APR is more relevant. It shows the simple cost of borrowing without compounding. Knowing the difference helps you compare financial products accurately. This knowledge can prevent mistakes and help you plan your savings and loans wisely. By keeping APY and APR clear in your mind, you can make informed decisions and manage your money confidently.

How Is APY Calculated?

Now that you understand what APY is, let’s talk about how it’s actually calculated. I won’t go too deep into complicated math, but I’ll give you enough so that you understand the process.

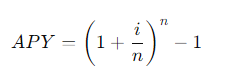

The formula to calculate APY is

Where:

- i is the interest rate (or APR),

- n is the number of compounding periods per year.

This formula might look a bit intimidating at first, but let me walk you through it.

- Interest Rate (i): The APR or nominal interest rate is the base rate your bank or investment offers before accounting for compounding.

- Compounding Periods (n): This refers to how often interest is added to your account. The more often interest is compounded (daily, monthly, quarterly, etc.), the higher the APY will be because compounding gives you interest on top of your interest more frequently.

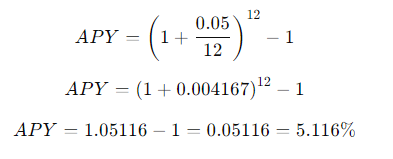

Let’s break it down with an example so you can see it in action. Imagine you have an account with a 5% interest rate (APR), and interest compounds monthly. In this case, your “n” would be 12 (since interest compounds 12 times per year).

Here’s what the calculation would look like:

So, in this example, even though the APR is 5%, the APY is 5.116% due to the effect of monthly compounding.

Factors That Affect APY

Several factors can influence APY, and knowing these will help you make informed decisions about your finances. Here’s what you should keep in mind:

- Interest Rate (APR): The higher the interest rate, the higher the APY will generally be.

- Compounding Frequency: As I mentioned earlier, the more frequently interest compounds, the higher your APY. Daily compounding will result in a higher APY than monthly or quarterly compounding, even if the APR stays the same.

- Length of Time: APY assumes that your money will stay in the account for a full year. If you withdraw your money before the year ends, you won’t earn the full APY. So, for accounts like CDs or fixed-term investments, it’s important to understand how long your money needs to stay in the account to benefit from the advertised APY.

- Fees: Some financial products come with fees that can lower your actual returns. Even if the APY looks great on paper, be sure to check if there are any maintenance or early withdrawal fees that could eat into your earnings.

- Minimum Balances: Many banks require a minimum balance to earn the advertised APY. If your balance falls below that minimum, you might earn a lower interest rate, which will result in a lower APY.

Comparing APY to Different Financial Products

APY is commonly used for savings accounts, CDs, and other interest-earning products, but it’s essential to compare APY when choosing between these options. Here’s a quick rundown of how APY plays a role in each:

1. Savings Accounts:

Traditional savings accounts offer a modest APY, usually ranging from 0.01% to 1%. While these accounts are safe and easy to access, the growth of your money can be very slow. For people who want their savings to earn more, the low APY may not be enough. Even though traditional accounts provide security, they often fail to keep up with inflation. This means your money’s purchasing power may decrease over time. Understanding the difference in APY between account types is important for anyone who wants to maximize their savings effectively.

On the other hand, high-yield savings accounts offer significantly higher APYs, sometimes 4% or more. In my experience, these accounts are ideal for building an emergency fund or growing short-term savings faster. The higher APY allows your money to compound more quickly, giving your savings a better chance to grow over time. Many high-yield accounts also have the same safety and accessibility as traditional accounts, making them a smart choice for cautious savers. By choosing a high-yield option, you can earn more interest without taking extra risks, helping your money work harder for you.

2. Certificates of Deposit (CDs):

Certificates of Deposit (CDs) often provide higher APYs than traditional or high-yield savings accounts. In exchange, you agree to lock up your money for a fixed term, which usually ranges from three months to five years. Generally, the longer the term, the higher the APY you can earn. This makes CDs a good option for money you do not need immediately. However, withdrawing funds before the term ends may result in early withdrawal penalties. To avoid losing interest, only use money in a CD that you are confident you will not need in the short term. By carefully choosing the term length and amount, CDs can be a reliable way to earn higher interest safely.

3. Money Market Accounts:

Money market accounts are a hybrid between savings and checking accounts, combining the best features of both. They typically offer higher APYs than traditional savings accounts, which helps your money grow faster over time. At the same time, they provide more access to your funds than a CD or high-yield savings account. Many money market accounts come with check-writing privileges or debit card access, giving you flexibility for everyday transactions. This makes them a great option for people who want to earn interest while still having access to their money when needed.

However, money market accounts often have higher minimum balance requirements to earn the top APY. If you fall below the required balance, your interest earnings may be lower. By maintaining the minimum balance, you can maximize your returns while keeping your funds relatively liquid. These accounts are ideal for savers who want a balance of growth and accessibility without locking their money away. For anyone looking to grow their savings efficiently while retaining flexibility, a money market account can be a smart and practical choice.

See; How to Set Financial Goals for Your Future

How to Maximize APY in Your Financial Strategy

Understanding APY is just the first step. To make the most of it, you need to know how to incorporate it into your financial strategy.

- Shop Around for the Best Rates: When it comes to APY, not all financial institutions are created equal. Take the time to compare rates across banks and credit unions. You’d be surprised how much difference even a small percentage increase can make over time.

- Look for High-Yield Accounts: High-yield savings accounts are a great option if you’re looking to maximize APY. Many online banks offer significantly higher APYs compared to traditional brick-and-mortar banks. I’ve personally found that moving my savings to an online high-yield account made a noticeable difference in how quickly my money grew.

- Choose the Right Compounding Frequency: If you have the option, choose accounts that offer daily compounding over those that compound monthly or quarterly. As we’ve seen, the more frequently your interest compounds, the higher your APY, and the more money you’ll earn over time.

- Keep an Eye on Fees and Minimum Balances: To truly benefit from APY, you need to avoid fees and ensure you maintain the required minimum balance. Even the best APY won’t help you much if fees are eating into your earnings or if you aren’t keeping enough money in the account to qualify for the advertised rate.

Conclusion

By now, you should have a clear understanding of what APY is, how it is calculated, and why it matters. Whether you are saving for a rainy day, building an emergency fund, or investing for the long term, paying attention to APY can help you make smarter financial decisions. APY shows the real return on your money, including the effects of compound interest. This makes it easier to compare savings accounts, high-yield accounts, CDs, and investment products accurately. By focusing on APY, you can identify the accounts that will grow your money faster and choose the options that fit your financial goals.

It’s also important to know that APY isn’t just for the wealthy or professional investors. Anyone with a savings account, high-yield account, or investment product can benefit from understanding it. Monitoring APY allows you to maximize earnings, grow your savings efficiently, and make informed choices about where to put your money. The next time you are comparing financial products, take a close look at the APY. It is one of the most important numbers for evaluating your real return on investment. By understanding APY and how it works, you are now better equipped to manage your finances and grow your wealth confidently over time.